Business Succession Planning

By Steven D. Brett, Managing Director, Partner, Marcum Wealth

When developing a succession plan for your business, you must make many decisions. Should you sell your business or give it away? Should you structure your plan to go into effect during your lifetime or at your death? Should you transfer your ownership interest to family members, co-owners, employees, or an outside party? The key is to pick the best plan for your circumstances and objectives, and to seek help from financial and legal advisors to carry out this plan.

Selling your business

Selling your business outright

You can sell your business outright, choosing the right time to sell–now, at your retirement, at your death, or anytime in between. The sale proceeds can be used to maintain your lifestyle, or to pay estate taxes and other final expenses. As long as the price is at least equal to the full fair market value of the business, the sale will not be subject to gift taxes. But, if the sale occurs before your death, it may result in capital gains tax.

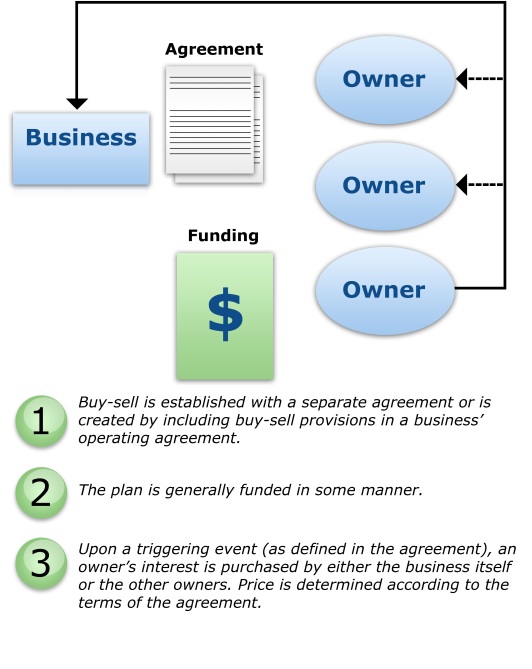

Transferring your business with a buy-sell agreement

A buy-sell is a legally binding contract that establishes when, to whom, and at what price you can sell your interest in a business. A typical buy-sell allows the business itself or any co-owners the opportunity to purchase your interest in the business at a predetermined price. This can help avoid future adverse consequences, such as disruption of operations, entity dissolution, or business liquidation that might result in the event of your sudden incapacity or death. A buy-sell can also minimize the possibility that the business will fall into the hands of outsiders.

The ability to fix the purchase price as the taxable value of your business interest makes a buy-sell agreement especially useful in estate planning. Agreeing to a purchase price can minimize the possibility of unfair treatment to your heirs. And, if your death is the triggering event, the IRS’ acceptance of this price as the taxable value can help minimize estate taxes.

Additionally, because funding for a buy-sell is typically arranged when the buy-sell is executed, you’re able to ensure that funds will be available when needed, providing your estate with liquidity that may be needed for expenses and taxes.

Private annuity

With a private annuity, you transfer your ownership interest in the business to family members or another party (the buyer). The buyer in turn makes a promise to make periodic payments to you for the rest of your life (a single life annuity) or for your life and the life of a second person (a joint and survivor annuity). Again, because a private annuity is a sale and not a gift, it allows you to remove assets from your estate without incurring gift or estate taxes.

Until 2006, exchanging property for an unsecured private annuity allowed you to spread out any gain realized, deferring capital gains tax. IRS regulations proposed that year have effectively eliminated this benefit for most exchanges, however. If you’re considering a private annuity, be sure to talk to a tax professional.

Self-canceling installment note

A self-canceling installment note (SCIN) allows you to transfer your interest in the business to a buyer in exchange for a promissory note. The buyer must make a series of payments to you under that note, and a provision in the note states that at your death, the remaining payments will be canceled. Like private annuities, SCINs provide for a lifetime income stream and they avoid gift and estate taxes. But unlike private annuities, SCINs give you a security interest in the transferred business.

Gifting your business

If you’re like many business owners, you’d prefer to have your children inherit the result of all your years of hard work and success. Of course, you can bequeath your business in your will, but transferring your business during your lifetime has many additional personal and tax benefits. By gifting the business over time, you can hand over the reins gradually as your offspring become better able to control and manage the business on their own, and you can minimize gift and estate taxes.

Gifting your business interests can minimize gift and estate taxes because:

- It transfers the value of any future appreciation in the business out of your estate to your heirs. This can be especially valuable if business growth is expected.

- Gifts of $14,000 (in 2014 and 2015) per recipient are tax free under the annual gift tax exclusion.

- Aggregate gifts up to $5,430,000 (in 2015, $5,340,000 in 2014) are tax free under your lifetime exemption.

- Partial interest gifts, as with GRATs, GRUTs, and FLPs, may be valued at a discount for lack of marketability or restrictions on transferability.

Gifting your business using trusts

You can make gifts outright or use a trust. You can even structure a trust so that you keep control of the business for as long as you want. You can establish a revocable trust, which will bypass probate and allow you to change your mind and end the trust, or an irrevocable trust, such as a grantor retained annuity trust (GRAT) or a grantor retained unitrust (GRUT) that can provide you with income for a specified period of time and move your business out of your estate at a discount.

Gifting your business using a family limited partnership

You can transfer your business interest using another entity, such as a family limited partnership (FLP). An FLP is a limited partnership formed to manage and control a family business. You (and your spouse) can be the general partners, retaining control of the business itself and receiving income from the business, while your children can be limited partners.

By transferring the business to an FLP, you may be able to use valuation discounts and substantially reduce the value of the business for tax purposes by making annual gifts to the limited partners.

This material was prepared by Raymond James for use by Steven D. Brett, President of Marcum Financial Services LLC., and Branch Manager of Raymond James Financial Services, Inc. Member FINRA/SIPC.If you have any questions pertaining to this article, please contact Steven D. Brett at 631-414-4020 or by e-mail at [email protected].

This information, developed by an independent third party, has been obtained from sources considered to be reliable, but Raymond James Financial Services, Inc. does not guarantee that the foregoing material is accurate or complete. This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. This information is not intended as a solicitation or an offer to buy or sell any security referred to herein. Investments mentioned may not be suitable for all investors. The material is general in nature. Past performance may not be indicative of future results. Raymond James Financial Services, Inc. does not provide advice on tax, legal or mortgage issues. These matters should be discussed with the appropriate professional.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC, an independent broker/dealer, and are not insured by FDIC, NCUA or any other government agency, are not deposits or obligations of the financial institution, are not guaranteed by the financial institution, and are subject to risks, including the possible loss of principal.