Control v. Non-Controlling Level of Value

By Kenneth J. Pia, Jr., Partner, Business Valuation Industry Leader

Valuation theory is predicated on the notion that the level of control attaching to common stock has a direct and empirically observable impact on the value of the stock. That said, it is necessary and appropriate in each case to consider the actual level of control in evidence. In establishing the level of control we look to what we refer to as the facts and circumstances test; there is no rule of thumb or magic formula that will suffice.

Also, the notion that value attaches to control should be no less true for one type of company than another, i.e. an Employee Stock Ownership Plan (“ESOP”) owned company, as opposed to a plain vanilla corporation. That notion simply has no support within business valuation theory. However, recently a number of rulings by the Department of Labor (“DOL”) and various courts have clouded the issue. We have seen decisions recognizing control wherein none can be said to exist, and quite the opposite as well. Under the circumstances, valuation advisors need to be mindful of the need to stay within the Fair Market Value (“FMV”) standard of value. Because the FMV standard makes clear that the hypothetical willing buyer and seller are knowledgeable parties that are willing and able to transact, it seems clear that they would consider the level of legal and operating control held by an ESOP trust.

In any valuation, including ESOP valuations, consideration of the level of control should include a review of the company’s governing legal documents with an eye towards detecting control issues. The analysis should consider the powers of the board of directors and shareholders; the election and removal of directors; the filling of vacancies on the board; the ability to amend the legal documents; and, any other matter that might impact control. For example, the ESOP may hold 100%, or a majority of the voting stock, but may be allowed to appoint only a minority of the board of directors. Or perhaps election of directors is by a plurality of the vote, and the ESOP is one of several stockholders despite owning a majority in interest of the voting stock. In these ways and others, including guaranteed board seats for ESOP selling stockholders, a shareholder owning a majority of the voting stock may not have legal control of the company. There is also the issue of whether, and to what extent, the trustee is directed, which is a particular issue in ESOP companies with internal trustees. While fiduciary responsibilities may to some extent mitigate lack of control for directed trustees, it is typically considered as a last resort.

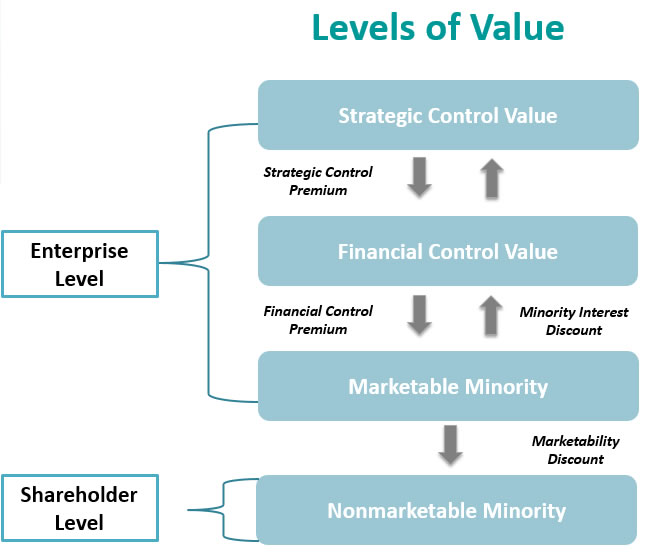

Control, or lack thereof, can be reflected in a valuation by applying a discount or premium to value, or in certain circumstances using valuation conventions that represent a controlling or non-controlling basis. These elements might include the use of control or minority cash flows and the adjustment of the capital structure used in the valuation. Examples of controlling adjustments to the cash flow include normalizing owner/officer compensation or other related-party payments to market rates, while capital structure factors may include whether the cost of debt and weighting of debt in the capital structure are set to industry-optimal measures.

A discount for lack of control (“DLOC”) for a controlling interest, or not adjusting owner/officer compensation to market, is not only counter-intuitive but is potentially in violation of the FMV standard and other relevant professional standards. We must be careful that we do not find ourselves creating a special form of ESOP FMV which is not supported by sound logic, professional standards or governmental regulations, including those of the DOL. If the ESOP has legal control of the entity as demonstrated in the legal documents, but is not exercising that control, that is not a reason to value the ESOP stock on a non-controlling basis. Perhaps there needs to be more board/management/trustee interaction prior to encountering a situation wherein the CEO or president can simply pay his or her self a hefty bonus, or increase their own compensation, even if it is completely warranted; in other words, setting parameters proactively to reward management for their contributions in increasing value to the owners/participants.

The accepted levels of value in the business valuation profession look something like this:

*Source: AAML Annual Meeting – November 2-5, 2016 Renaissance Hotel, Chicago, IL

This is certainly not the only circumstance where FMV is viewed and applied differently by agencies of the U.S. government. Tax-affecting with respect to the valuation of S corporations for ESOP administration purposes as overseen by the DOL, and for estate and gift tax purposes as overseen by the Internal Revenue Service is another example. The DOL insists on tax-affecting and the IRS comes down strongly against it.

Are we losing the forest for the trees? Are we, as valuation professionals, expected to view things differently for transactions as opposed to annual updates for purposes of calculating participant value for redemptions? Are we expected to use differing conventions in valuing ESOP companies, as opposed to non-ESOP S corporations? There exists neither theoretical support nor empirical evidence that supports such a notion. The job of the valuation professional is to follow the FMV standard; in the area of understanding the impact of control recognize that what we refer to as the facts and circumstances test is a polite way to say that the devil is in the details.