An Explanation of the Market Approach to Valuation – Guideline Public Company Method

By Sean R. Saari, Partner, Advisory Services

Investors in publicly-traded companies have the luxury of knowing the value of their investment at virtually any time. An internet connection and a few clicks of a mouse are all its takes to get an up-to-date stock quote. Of all U.S. companies, however, less than 1% are publicly-traded, meaning that the vast majority of companies are privately-held. Investors in privately-held companies do not have such a readily available value for their ownership interests. How are values of privately-held businesses determined, then? Each month, this eight blog series will answer that question by examining a key component of how ownership interests in privately-held companies are valued.

Market Approach

There are two market approaches that are primarily used when valuing a business, the Guideline Transaction Method and the Guideline Public Company Method. These methods are used to value a company based on the pricing multiples observed for similar companies that were sold or are publicly-traded.

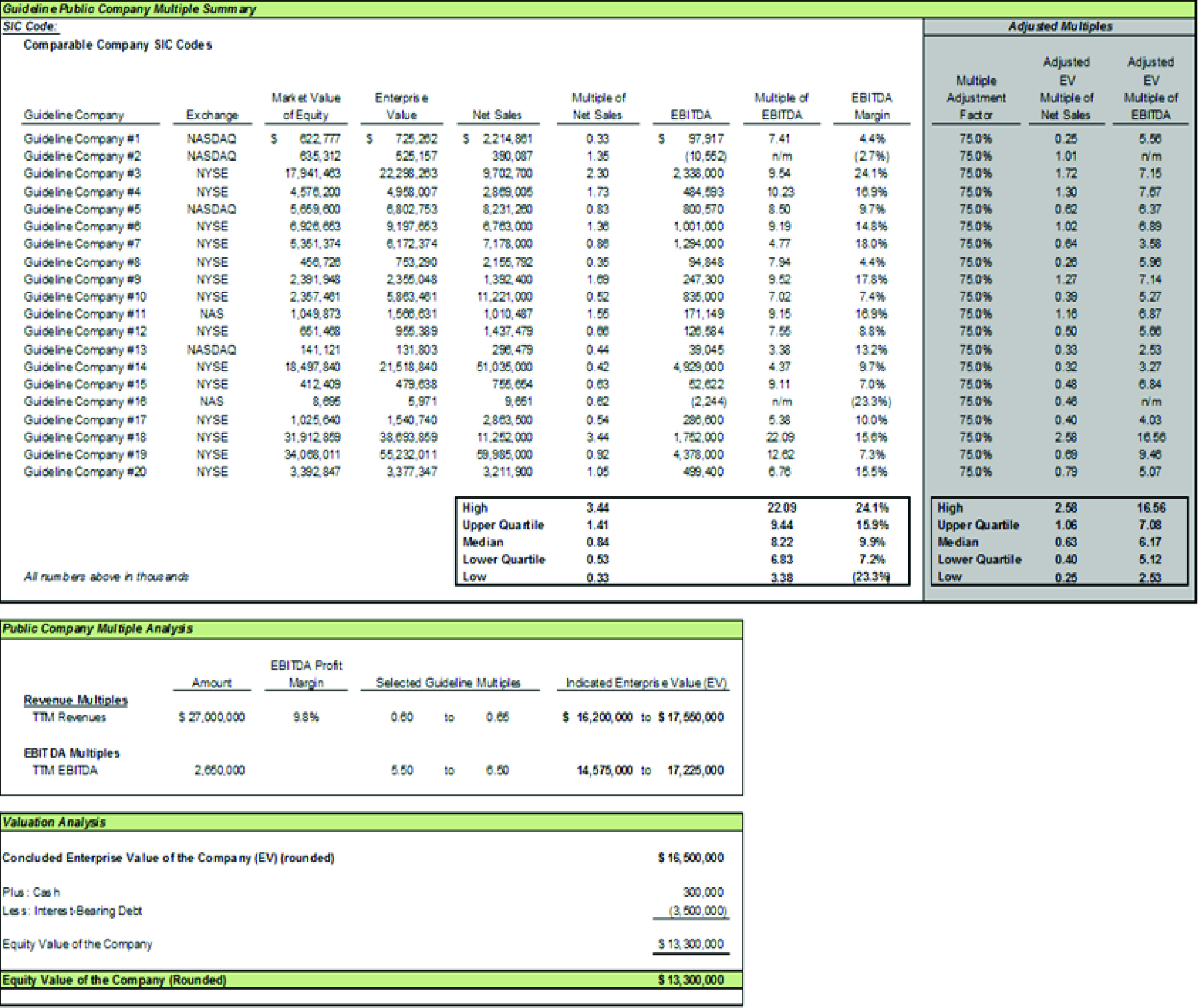

More information related to the Guideline Public Company Method is provided below along with example:

Guideline Public Company Method – The Guideline Public Company Method values a business based on trading multiples derived from publicly traded companies that are similar to the subject company. The steps taken in applying the Guideline Public Company Method include identifying comparable public companies, adjusting the guideline public company multiples for differences in the size and risk of these companies compared to the subject company, and then applying the adjusted pricing multiples from the representative companies.

Ideally, the guideline public companies selected for analysis compete in the same industry as the subject company. When such publicly-traded companies do not exist (or when only a small number of them exist), other companies with similar underlying characteristics such as markets serviced, growth, risks or other relevant factors can be considered – exact comparability is not required under this method of valuation, although closer comparables are preferred.

As mentioned above, the guideline public company multiples may be adjusted for differences in the size and risk of the guideline companies compared to the subject company being valued. Typically, this results in a downward adjustment to the guideline public company multiples.

Similar to the Guideline Transaction Method, the guideline public companies differ from the subject company in their respective stages of development and size, but they have comparable operational models and financial risks. They also reflect the economic conditions of the industries in which the subject company operates. Thus, the comparative analysis to the subject company being valued is based on the performance and characteristics of the sample as a whole rather than on any individual guideline company selected.

Also similar to the Guideline Transaction Method, the calculated multiples are often based on the enterprise values of the guideline public companies, meaning that we arrive at an enterprise value of the subject company when using the Guideline Public Company Method. Therefore, one must subtract debt and add cash to the calculated enterprise value to arrive at the company’s equity value.

An example of the Guideline Public Company Method is presented below:

To learn more about our Valuation services offered at Marcum LLP, contact Sean Saari at 440-459-5700.