Fed Changes Its Tune

By Michael McKeown, CFA, CPA, Chief Investment Officer, Marcum Wealth

The Federal Reserve has a problem.

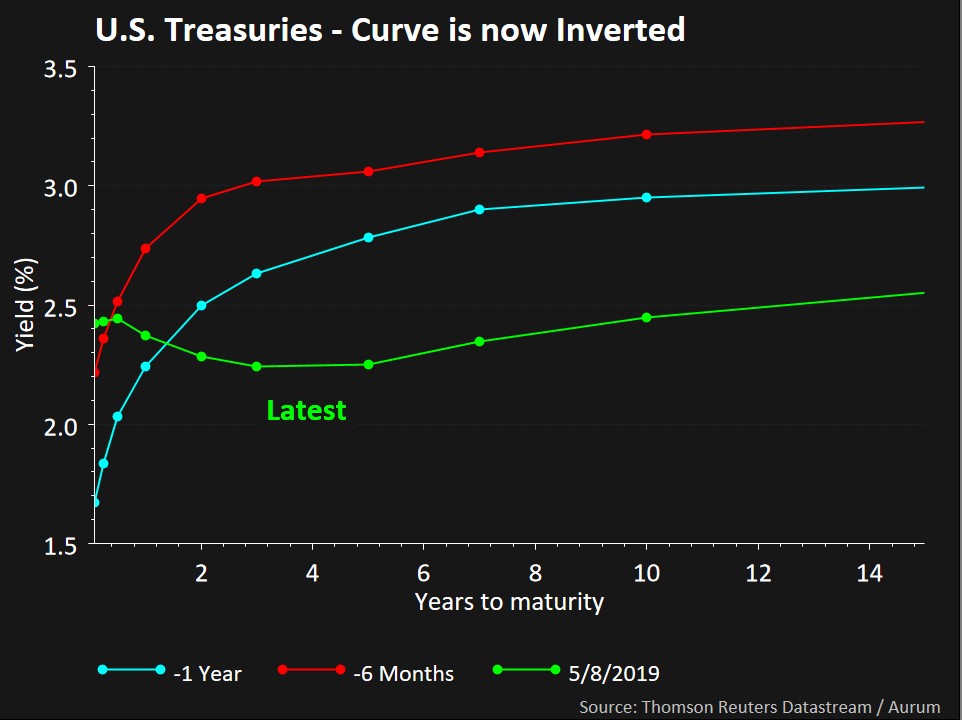

The yield curve is inverted. Meaning long-term rates are lower than short-term rates.

The Fed funds rate (set by the Fed) is essentially at the same level as the 10-year Treasury bond. The 2-year, 3-year, and 5-year Treasury bond rate is well below this around 2.3% (see neon green line). The shape is much different than 6 months (red line) or even a year ago (blue line). Looking back, the 10-year yield was north of 3% and all of these interst rates were higher. The yield curve was steeper.

What does it mean?

The bond market is telling the Federal Reserve that policy is too tight, betting that short-term interest rates have risen too far and too fast.

Admitting mistakes is tough, and the Fed probably did not need to raise interest rates in September and December of last year. The committee that sets rates needs intellectual cover on how to change the shape of the curve and lower interest rates.

Enter inflation targeting.

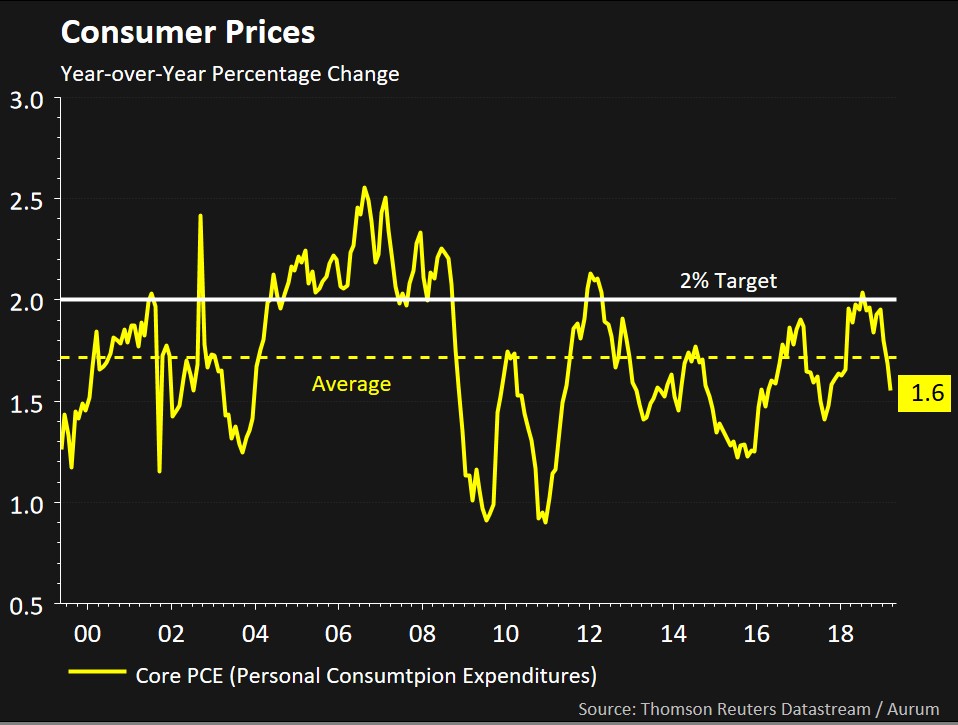

In 2012, the Fed set an inflation target of 2%. It cannot seem to get there.

The target is measured by the Core Personal Consumption Expenditures (PCE) index. Since then, inflation averaged 1.6%, right in line with its latest reading. Since the inception of this measure, it averaged 1.7%.

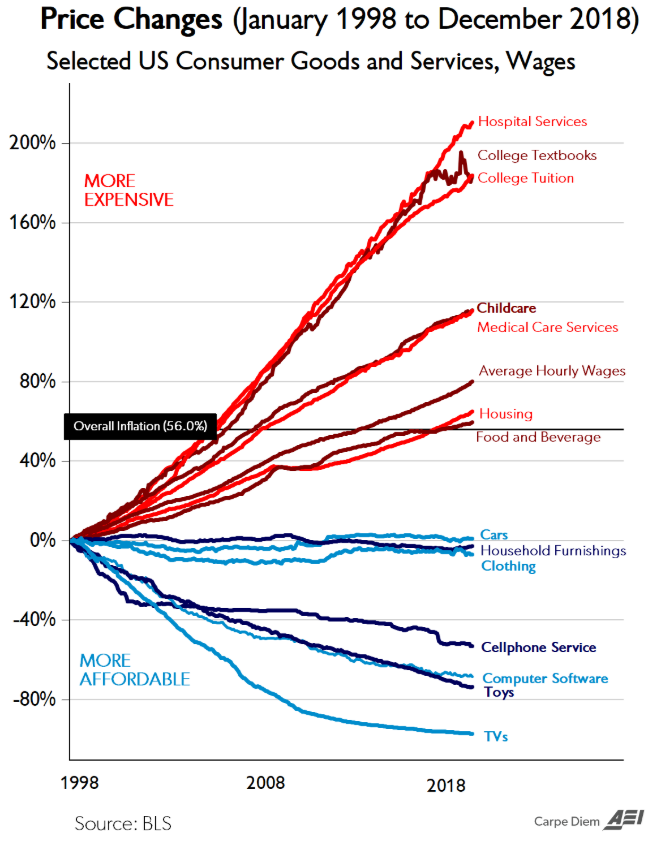

Some may be thinking, “I wish the stuff I bought only went up about 1% to 2% a year.” The following chart shows how various consumer goods and services have changed in price over the last 20 years. Many are much higher than a 2% per year increase.

The Fed missing its 2% target by a few tenths of a percent does not sound like much, especially faced with the 200% increase in healthcare costs.

However, it is a big enough issue that they have been holding discussions and roundtables around the country the last few months. They need to figure out how to get inflation up!

This culminates in the Conference on Monetary Policy, scheduled for June 4th and 5th. One possible way to change policy is using an average of inflation over time, allowing it to rise above 2% in good times, perhaps as high as 2.5%. Since it has fallen below 1.5% in economic slowdowns and recessions, this would allow the average to be 2% over a cycle. This could be the biggest change in Fed policy in eight years.

The policy being discussed is averaging inflation over a period time. This gives them reason to keep monetary policy easier (and even lower interest rates), which is what the bond market is pricing in by early 2020.

With tariffs taking center stage again, the Fed is watching for signs of slowing growth and inflation missing its target. If data disappoints, it gives them enough reason to call for a ‘maintenance interest rate cut.’

While just six months ago, the bond market was thinking about 2 to 3 hikes in 2019. Now a rate cut is on the table.

The yield curve controls Fed policy. We are seeing that in action today.

Questions about this blog? Contact Michael McKeown, CFA, CPA – Chief Investment Officer.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Marcum Wealth, or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Marcum Wealth. Please remember to contact Marcum Wealth, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Marcum Wealth is neither a law Firm, nor a certified public accounting Firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the Marcum Wealth’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request. Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Marcum account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Marcum accounts; and, (3) a description of each comparative benchmark/index is available upon request.