The Pass-Through Entity Tax: A SALT Limitation Workaround

By Adam Wachler, CPA, Tax Senior Manager, Alternative Investments Group

When the Tax Cuts and Jobs Act (TCJA) was passed in 2017, it limited state and local tax (SALT) deductions for individuals to just $10,000. Companies and individuals in states with higher tax rates, like New York at 12.75%, were adversely affected by the legislation. Many states looked for ways to work around the limitation and encourage individuals to do business and reside in their state. Eventually, the pass-through entity tax (PTET) became the primary strategy for partnerships working around this $10,000 SALT cap.

Although the TCJA limited the state and local tax deduction for individuals, it still allows entities such as partnerships to deduct state and local taxes. The PTET election moves the tax from the individual level to the entity, allowing for the full deduction (which is ultimately passed through to the individual). Depending on the state, an investor then claims a credit for the tax paid, or their adjusted gross income is reduced by their share of the income received from an electing pass-through entity (PTE).

The IRS released Notice 2020-75 in late 2020, allowing the PTET deduction to be taken at the entity level and passed through to an investor. The notice does not clearly state the types of businesses allowed to take these deductions. If you are operating a trade or business, you are entitled to make an election and deduct the state and local taxes. The notice also doesn’t mention if entities such as investment partnerships that earn non-business income are entitled to these deductions. This is one reason it is essential to consult with a tax advisor before making any PTET election.

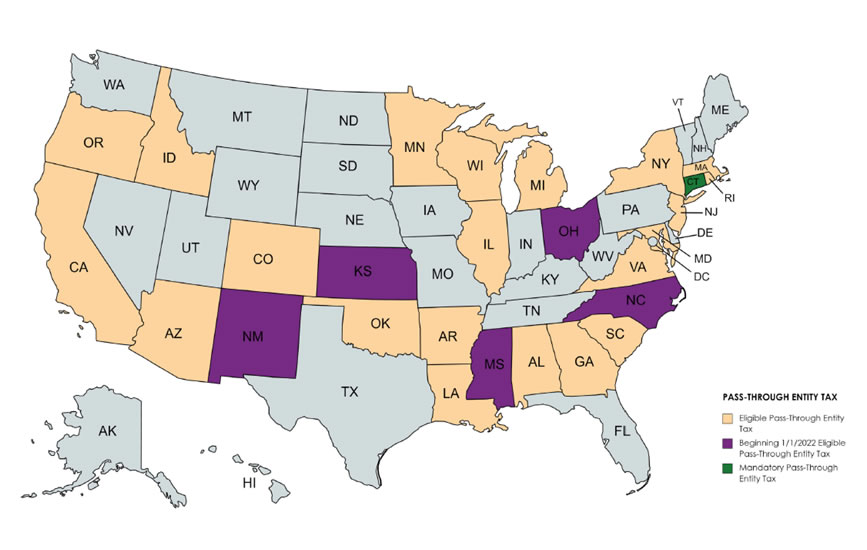

Where PTET Elections Can Be Made

Below is a map that shows all of the states that currently allow a PTET election, as well as ones that will enable it starting in 2022. New York City will also allow the PTET election beginning January 1, 2023. The New York City pass-through entity tax is in addition to all other current taxes, including the Unincorporated Business Tax.

New York Pass-Through Entity Tax

The New York State PTET is an annual irrevocable election. For years 2022 or later, the election must be made between January 1 and March 15. To assist, New York has extended the election period for 2022 until September 15. The PTET graduated rate ranges from 6.85% to 10.9%. The credit is only available for partners — such as individuals, estates, and trusts — subject to tax under Article 22. For any pass-through entity tax imposed by another state, New York will permit a resident tax credit against New York State personal income tax.

Connecticut Pass-Through Entity Tax

As seen on the map above, the only mandatory pass-through entity tax is imposed in Connecticut. The tax is levied on any partnership or S-corporation that does business in Connecticut or has income derived from or connected with Connecticut sources. All partners in a partnership are subjected to the 6.99% tax.

New Jersey Pass-Through Business Alternative Income Tax (PTE/BAIT)

The New Jersey Pass-Through Business Alternative Income Tax election is an annual election that must be made on the due date of the tax return. The PTE/BAIT applies to all entities, and the partner receives a credit of 100% of the tax paid. In 2022, an electing PTE pays tax on its NJ taxable income at a graduated tax rate ranging from 5.675% to 10.9%, depending on its distributive proceeds.

California Pass-Through Entity (PTE) Elective Tax

The California PTE is an annual irrevocable election made on a timely filed tax return. The PTE elective tax applies to individuals, fiduciaries, estates, or trusts subject to California personal income tax, and to disregarded entities owned by one of the former. The elective tax is 9.3% of the entity’s qualified net income, which is the sum of the qualified taxpayer’s income subject to California personal income tax. A qualified taxpayer can carry forward the nonrefundable credit for up to five years.

While making a PTET election could be in the best interest of an entity, the outcome varies significantly depending on the state and many other variables. It is necessary to consult with a tax advisor to determine the impact any PTET elections will ultimately have on the entity and its investors.