The Income Approach to Valuation – Discounted Cash Flow Method

By Sean R. Saari, Partner, Advisory Services

Investors in publicly-traded companies have the luxury of knowing the value of their investment at virtually any time. An internet connection and a few clicks of a mouse are all its takes to get an up-to-date stock quote. Of all U.S. companies, however, less than 1% are publicly-traded, meaning that the vast majority of companies are privately-held. Investors in privately-held companies do not have such a readily available value for their ownership interests. How are values of privately-held businesses determined, then? Each month, this eight blog series will answer that question by examining a key component of how ownership interests in privately-held companies are valued.

Income Approach

There are two income-based approaches that are primarily used when valuing a business, the Capitalization of Cash Flow Method and the Discounted Cash Flow Method. These methods are used to value a company based on the amount of income the company is expected to generate in the future.

The Capitalization of Cash Flow Method is most often used when a company is expected to have a relatively stable level of margins and growth in the future – it effectively takes a single benefit stream and assumes that it grows at a steady rate into perpetuity. The Discounted Cash Flow method, on the other hand, is more flexible than the Capitalization of Cash Flow Method and allows for variation in margins, growth rates, debt repayments and other items in future years that may not remain static. As a result, the Capitalization of Cash Flow Method is typically applied more often when valuing mature companies with modest future growth expectations. The Discounted Cash Flow Method is used when future growth rates or margins are expected to vary or when modeling the impact of debt repayments in future years (although it can still be used in same sort of “steady growth” situations in which the Capitalization of Cash Flow Method can be applied).

More information related to the Discounted Cash Flow Method is provided below along with an example:

Discounted Cash Flow Method – The Discounted Cash Flow Method is an income-based approach to valuation that is based upon the theory that the value of a business is equal to the present value of its projected future benefits (including the present value of its terminal value). The terminal value does not assume the actual termination or liquidation of the business, but rather represents the point in time when the projected cash flows level off or flatten (which is assumed to continue into perpetuity). The amounts for the projected cash flows and the terminal value are discounted to the valuation date using an appropriate discount rate, which encompasses the risks specific to investing in the specific company being valued. Inherent in this method is the incorporation or development of projections of the future operating results of the company being valued.

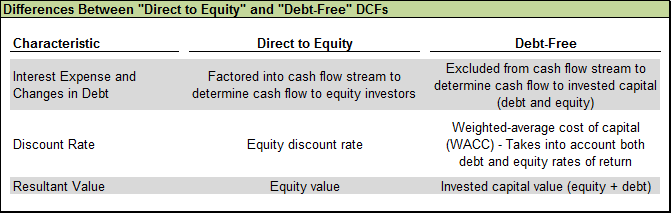

Distributable cash flow is used as the benefit stream because it represents the earnings available for distribution to investors after considering the reinvestment required for a company’s future growth. The discounted cash flow method can be based on the cash flows to either a company’s equity or invested capital (which is equal to the sum of a company’s debt and equity). A “direct to equity” discounted cash flow method arrives directly at an equity value of a company while a “debt-free” discounted cash flow method arrives at the invested capital value of a company, from which debt must be subtracted to arrive at the company’s equity value. A brief summary of some of the primary differences between a “direct to equity” and a “debt-free” discounted cash flow analysis are presented below:

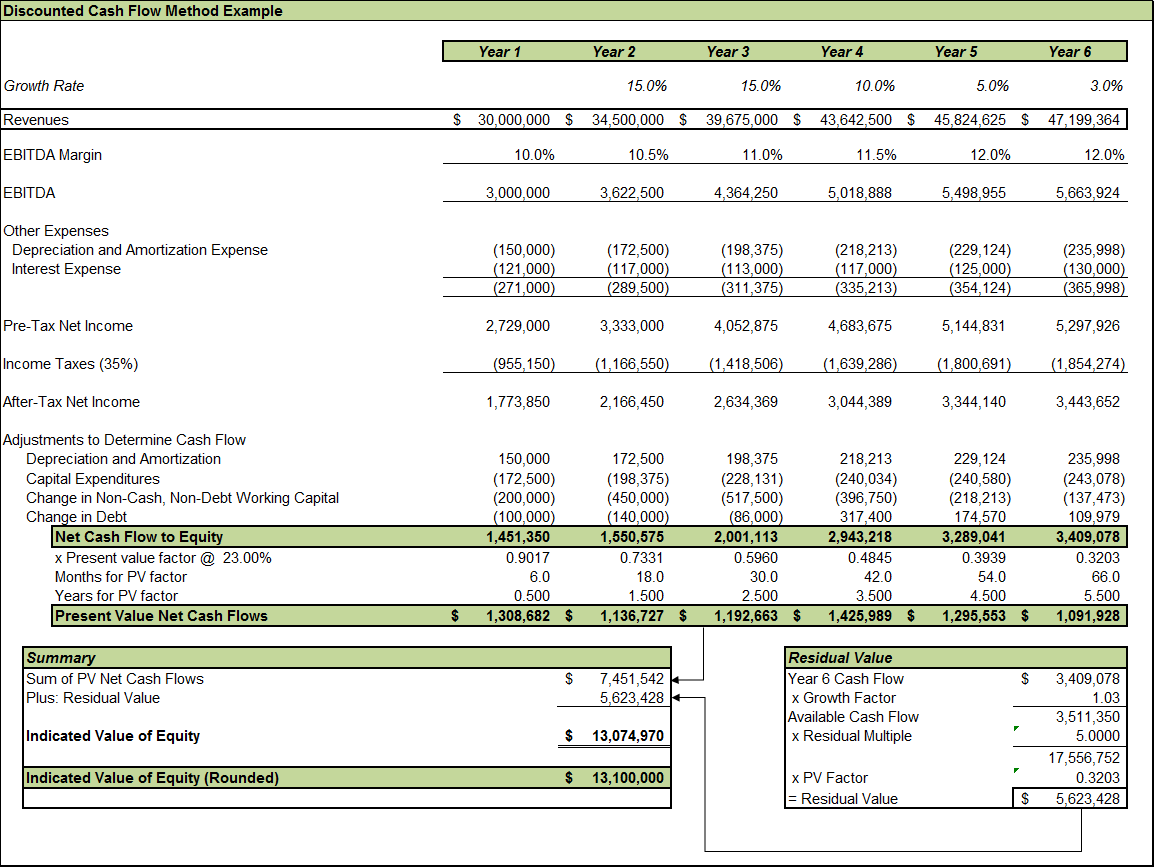

An example of a “direct to equity” discounted cash flow analysis is presented below:

To summarize, the Discounted Cash Flow Method is an income-based approach to valuation that is based on the company’s ability to generate cash flows in the future.

For more information on valuations, contact Sean Saari at 440-459-5865 or [email protected].