Nonresidential Construction Recovery Restrained in First Quarter, Construction Employment Improves

New York City, NY – Nonresidential construction spending retrenched in the first quarter of 2013 despite an expansion of the U.S. economy and an improving housing market, according to the quarterly Marcum Commercial Construction Index released today by Marcum LLP. The positive performance of both economic indicators produced a modest improvement in construction employment.

Nonresidential Fixed Investment in Structures for the first quarter declined 0.3 percent, even as U.S. Gross Domestic Product (GDP) increased 2.5 percent. The first quarter commercial construction decline compares to a gain of 16.7 percent in the fourth quarter of 2012 and 12.9 percent in the first quarter last year.

“Neither public nor private construction has exhibited significant upward momentum of late. In fact, the year-over-year comparisons deteriorated in March for both categories,” said Anirban Basu, Marcum’s Chief Construction Economist and chairman of Sage Policy Group, a leading economic advisor to the construction industry.”“Federal sequestration impacts will become more apparent during the second quarter. As a result stakeholders can expect the recovery in nonresidential construction to remain highly constrained with rare industry-specific and geographic exceptions. Sequestration is expected to result in more than $4 billion in cuts to ongoing construction programs, and there will be additional indirect or multiplier effects.”

Construction Spending

The first quarter of 2013 ended on a downturn, with nonresidential construction spending in March falling 2.9 percent on a seasonally adjusted basis, following a 1.2 percent increase in February and a 4.3 percent reduction in January. The March nonresidential performance compares to an increase of 0.7 percent in residential construction spending the prior month.

Year-over-year, total construction spending in March was up 4.8 percent, but fell off 1.7 percent from February. In the nonresidential category, spending declined 1.2 percent year-over-year, while year-to-year residential spending jumped 17.8%.

Reflecting the overall downward trend, 11 out of 16 nonresidential sub-sectors posted losses, including sewage and waste disposal, down 18.8 percent; public safety, down 14.3 percent; and amusement and recreation, down 12.9 percent. Bright spots were, again, in transportation (up 19.1 percent), lodging (up 11.6 percent) and power (up 4.3 percent) year-over-year.

Construction Employment

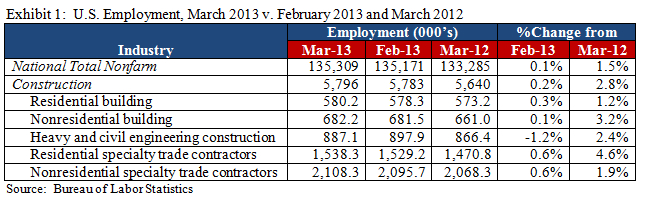

The just-reported total construction industry employment figures for April 2013 were virtually unchanged from the end of the first quarter, with a drop of 0.1 percent overall. Residential sector employment increased incrementally by 1.1%, versus a loss of 0.7 percent in the nonresidential category. Year-to-year, total construction employment in April increased 2.7 percent. Nonresidential construction employment marginally outpaced the residential sector, with increases of 2.7 percent and 2.5 percent, respectively.

The good news reported in April is consistent with trends demonstrated during the first quarter. March employment in nonresidential construction gained 3.2 percent year-over-year and 0.1 percent from February. Residential building employment had an annual gain of 1.2 percent, and a monthly gain of 0.3 percent.

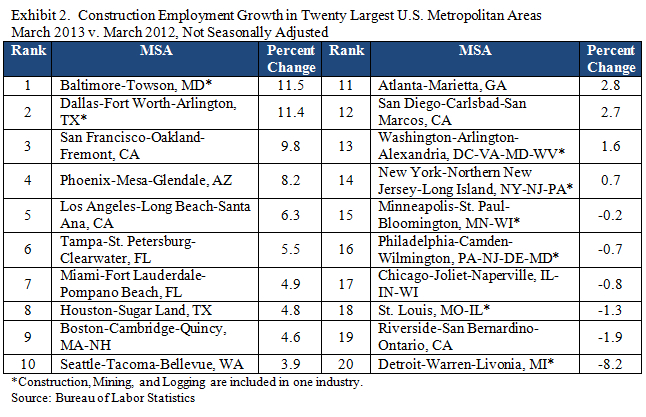

Fourteen of the 20 largest metropolitan areas in the country experienced new construction employment in March, led by Baltimore with year-over-year growth of 11.5 percent. Detroit, among other industrial Midwest cities, experienced the greatest loss of construction employment, which was down 8.2 percent.

“Looking back at the past three months, it seems we continue on the path of a slow but meaningful recovery within the construction sector. I note a cautious but continued optimism among my construction contractor clients and my peers in professional services. Times may not be getting better as quickly as we’d like, but the hard data is out there, showing signs of improvement. I am advising my clients to stick to these facts and build upon these successes,” said Marcum Construction Industry Group Leader Joseph Natarelli, Partner-in-Charge of the Firm’s New Haven Office.

“Various leading indicators such as the Architecture Billings Index remain in positive territory, implying nonresidential construction spending growth during the latter stages of 2013 and 2014. Many projects are in planning stages across many segments. However, the next several months are likely to be softer from a growth perspective than January and February,” Mr. Basu said.

About Marcum LLP

Marcum LLP is a top-ranked national accounting and advisory firm dedicated to helping entrepreneurial, middle-market companies and high net worth individuals achieve their goals. Marcum’s industry-focused practices offer deep insight and specialized services to privately held and publicly registered companies, and nonprofit and social sector organizations. The Firm also provides a full complement of technology, wealth management, and executive search and staffing services. Headquartered in New York City, Marcum has offices in major business markets across the U.S. and select international locations. #AskMarcum.