Deferring and/or Eliminating Capital Gains through Qualified Opportunity Zones

A New Federal Incentive Designed to Encourage Development in Low Income Areas.

One unique provision of the Tax Cut and Jobs Act (TCJA) of 2017 is a new federal incentive called Qualified Opportunity Zones (“QOZ”). The goal of this new provision is to encourage capital investment in certain low-income communities within the United States. The IRS has approved census tracts for all 50 states and the District of Columbia that qualify for Opportunity Zone investments.

The new provision allows capital gains that are “reinvested” in a Qualified Opportunity Zone Fund (“QOZF”) to be temporarily deferred from being included in the investor’s gross income.

A QOZF is an investment vehicle organized as a corporation or a partnership for the purpose of investing in a Qualified Opportunity Zone Property (“QOZP”) subject to certain requirements (below). QOZP includes any Qualified Opportunity Zone Stock (“QOZS”), Qualified Opportunity Zone Partnership Interest (“QOZPI”) or Qualified Opportunity Zone Business Property (“QOZBP”).

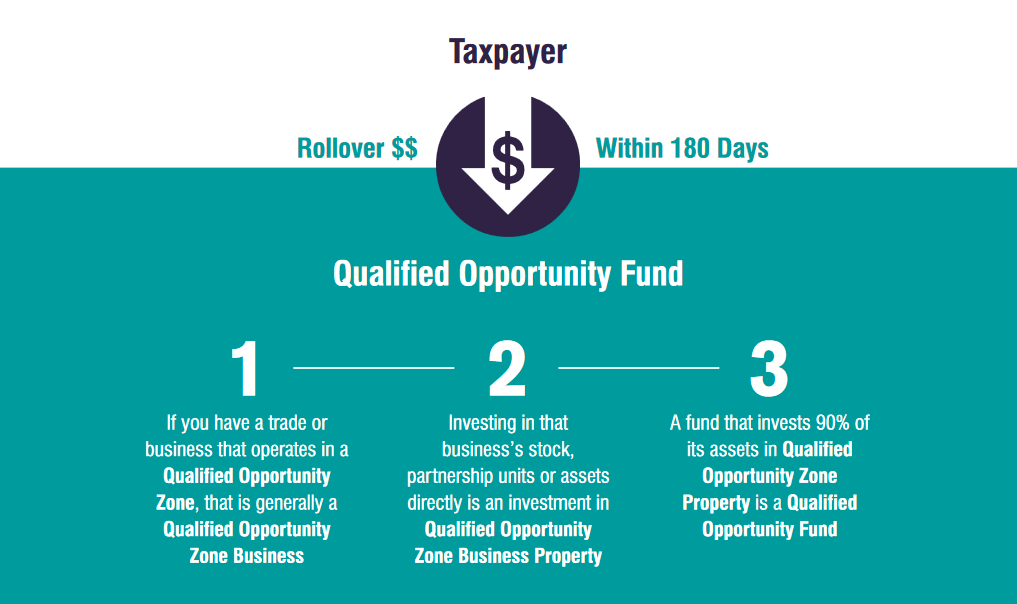

A taxpayer may defer up to 100% of realized capital gain if the capital gain is reinvested into a Qualified Opportunity Fund within 180 days from the date of the sale of the asset.

If the investment in the QOF is held by the taxpayer for at least five years, the basis is increased by 10% of the original deferred gain. If the taxpayer holds the investment for at least seven years, the basis is increased by an additional 5%. The deferred gain is recognized on the date on which the QOF investment is liquidated or December 31, 2026, whichever comes first.

The provision also excludes from gross income the post-acquisition capital gain on investments in QOZFs that are held for at least 10 years. For the sale of a QOZF investment held for more than 10 years, the taxpayer can make an election to convert the basis of such investment to the fair market value of the investment at the date of sale, thus creating no gain recognition. Taxpayers can continue to recognize losses associated with investments in QOZF.

How Does the Opportunity Zone Work?

There are three ways to invest in an Opportunity Zone in order to deferand/or eliminate capital gains:

- Qualified Opportunity Zone Business– If a trade orbusiness meets certain requirements, including maintainingsubstantially all of the tangible property used by the trade orbusiness within a Qualified Opportunity Zone ("QOZ"), it will bedesignated a Qualified Opportunity Zone Business ("QOZB").

- Qualified Opportunity Zone Property– If an investment ina QOZB is made by purchasing Qualified Opportunity ZoneStock ("QOZS"), a Qualified Opportunity Zone PartnershipInterest ("QOZPI"), or the tangible assets in a QualifiedOpportunity Zone Business Property ("QOZBP"), the investmentwill be considered a Qualified Opportunity Zone Property ("QOZP").

- Qualified Opportunity Fund- A fund that is set up as acorporation or a partnership and invests 90% of its assets inQualified Opportunity Zone Property is a Qualified OpportunityFund ("QOF"). The fund is subject to certain testing datesevery six months to ensure 90% of its assets remain in the QOZ.

ACTION STEPS

For further information or to verify whether an address is located inan Opportunity Zone, contact your Marcum professional.