Investing in Legal Cannabis

By Leslie Bocskor, President, Electrum Partners

Introduction

Right now, we are seeing a very rare occurrence in the history of the world’s economy: the transformation of black market cannabis into a regulated, lucrative, global industry.

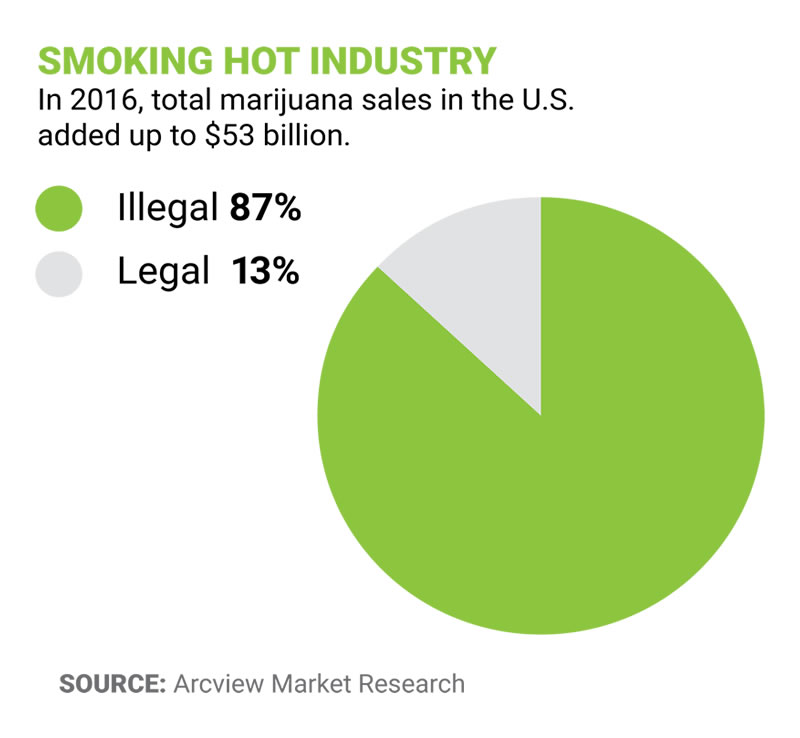

SOURCE: Arcview Market Research

The migration of a black market to a regulated market (according to studies by the UN and RAND Corp in 2010 of over $40 billion a year in adult use of cannabis only) is often compared to the end of prohibition of alcohol in 1933 and the repeal of the Volstead Act. The reasons for the comparisons are obvious. Both alcohol and cannabis can induce euphoric sensations, and both were prohibited. However, the parallels end there.

Here are the key differences:

- Alcohol was prohibited by the U.S. only. Meanwhile, liquor brands evolved internationally.

- Cannabis prohibition was exported to the rest of the world by the 1961 Single Convention on Narcotic Drugs treaty (the life’s work of Henry Jacob Anslinger, the architect of marijuana prohibition). Wiki: https://en.wikipedia.org/wiki/Harry_J._Anslinger

- The prohibition of cannabis also resulted in the prohibition of hemp. Wiki: https://en.wikipedia.org/wiki/Prohibition_in_the_United_States

When one considers the enormous markets for pharmaceuticals, nutraceuticals, supplements, and numerous therapeutic treatments, and the many conditions cannabis and hemp may be used to treat – such as pain management, insomnia, nausea, and eating disorders – it becomes clear that the opportunity is once in a lifetime. In fact, I would argue that, like pharmaceuticals, it is a trillion dollar industry.

I know what you’re thinking…how can I defend that?

Let’s do the math. By some estimates, the adult-use recreational market in the U.S. and Canada will be $40 billion. Now consider that the U.S. and Canada have a combined population of roughly 360 million people, which is less than half the size of the total population of Spanish and Portuguese-speaking countries which have a population of approximately 730 million people. Then if you factor in India, as another new market for legal cannabis with a total population of about 1.3 billion people, the total equates to around 2 billion people (when combined with Spanish and Portuguese-speaking populations), equaling almost six times the number of North Americans. And don’t forget, this does not take into account Eastern and Western Europe, Africa or Pacific Rim countries including Malaysia, Indonesia, Australia and more.

Bottom line, the end of cannabis prohibition on a global scale creates an absolutely massive market opportunity.

The Legal Cannabis Investment Opportunity in the U.S.

Historic changes in public policy can lead to massive valuation shifts, which in turn can present unprecedented opportunity for financial gain by first movers. The legal cannabis market in the U.S. today presents massive valuation shifts as well as challenges that require a 24-7 dedication to understanding the space and staying on top of its fast-paced innovation and regulatory complexity.

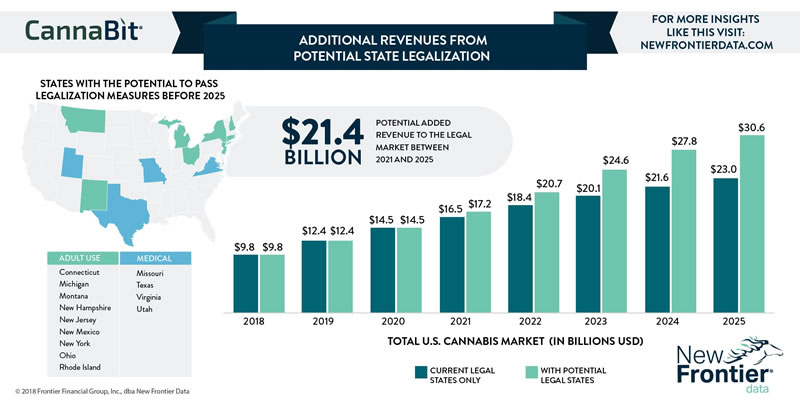

Similar to the end of prohibition for alcohol in the United States, the evolution of legalized medical and adult-use cannabis provides savvy investors with a window of opportunity for significant returns in a relatively short period of time as demonstrated in the chart below, which forecasts the potential market size when new US States will begin sales of medical and adult use cannabis.

Source: New Frontier Data

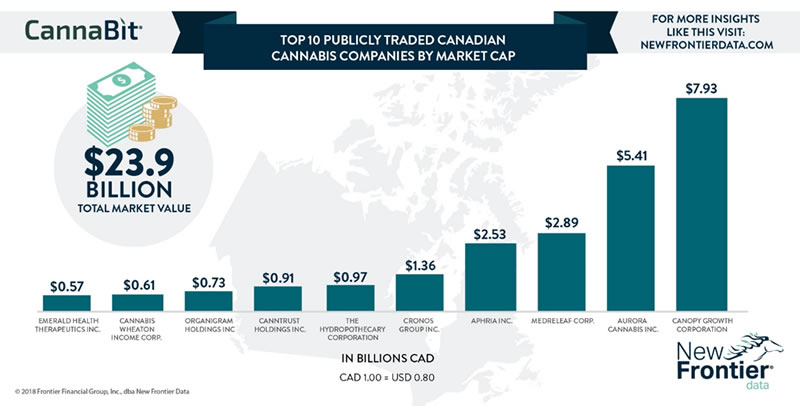

Canada provides a comparable as the country nears national legalization in October 2018. Cannabis company valuations are skyrocketing, as publicly traded Aurora and MedMen have seen astronomic growth through liquidity by listing on the CSE and then leveraging their position to scale up via strategic acquisitions. Canopy Growth Corporation has a market cap of $6.2 billion and Aurora is at $5.41 billion according to recent data from New Frontier.

Source: New Frontier Data

The Fragmented Market

In today’s marketplace, hyper-growth success stories like cannabis are rare, mainly because larger corporations traditionally possess superior market reach, large sales departments, and access to deep capital to fund the rollout of their products on a broad scale. Unfortunately, that’s not the typical case with the legal cannabis industry. Because of the federal illegality in the U.S., large national and multinational businesses are constitutionally locked out of the market. Federal law continues to classify cannabis as a Schedule I narcotic, a category reserved for drugs such as heroin – ones that are highly addictive and have no medical value – making the use, sale, and possession of all forms of cannabis in the United States (federally) illegal. This federal ban keeps national corporations and institutions on the side lines for now.

Currently, each state is weighing the pros and cons and developing regulatory frameworks independently, with some states only legalizing medical marijuana, and others going all in for adult use, while still others are refraining from legalization entirely. This creates a patchwork of rules and regulations within each state that legalizes cannabis for that state. Due to the newness of the industry and lack of consistent legal precedents in policy-making, challenges and obstacles may differ in each city and state due to the ringed fence nature of the industry. This is the fragmented market.

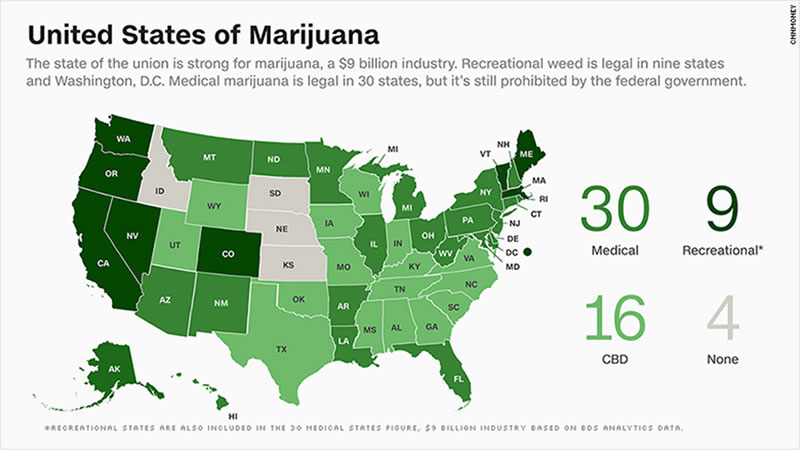

Source: BDS Analytics Data

The State of Legal Marijuana Markets, Sixth Edition published by Arcview Market Research in partnership with BDS Analytics.

Due to the ongoing federal prohibition, each state is forced to create its own “ringed fence” market, meaning that interstate commerce does not apply with regard to anything that touches the plant. Virtually every state is at a different stage in the evolutionary process of legalizing marijuana, with some states at full adult-use while others are just beginning to decriminalize the plant. Further, each state is also moving at a different pace from a regulatory perspective based on the formalized guidelines and legislative policies created by state policy makers. However, this also creates a window of opportunity.

The Advantage of a Fragmented Market for Investors

Normally, well-funded corporations have the upper hand in a regulated marketplace due to sheer scale and access to expansion funds via capital markets. However, because of a lack of competition at the national level, combined with the fragmented regulatory frameworks that are emerging in a staggered fashion, there is a unique blend of limitation and opportunity for savvy businesses to operate, safely insulated within the ringed fence economy of a deregulated state and temporarily protected from the competitive threat of much larger national players with unlimited resources entering the space.

Industries that are poised to enter the cannabis space include tobacco, liquor and pharmaceuticals, which all stand to gain because of their distribution infrastructures and massive economies of scale. They are also wise to hedge their current strength in the marketplace by gaining control of segments of the cannabis economy and limiting the potential for disruption. When you consider that the global pharmaceutical industry is projected to reach $1.12 trillion by 2022, the importance of a well-thought-out strategy for entering the legal cannabis space becomes evident. For example, studies have shown that when medical marijuana is legalized in a state with significant opioid addiction, opioid use generally declines as do the profits of the suppliers.

The fragmentation allows investors to identify best of breed companies with exceptional management teams, valuable IP, and established brands in large emerging growth markets, providing excellent returns through liquidity events as the industry matures.

The Cannabis Ecosystem

Once you really begin to drill down into each category, the scope of the opportunity is enormous. It’s a monstrous industry. In fact, I would argue that cannabis isn’t just one industry, but hundreds of industries converging into a large economic ecosystem comprised of cannabis companies that “touch the plant” and many others that are ancillary to the product. For experienced investors, there are a lot of options.

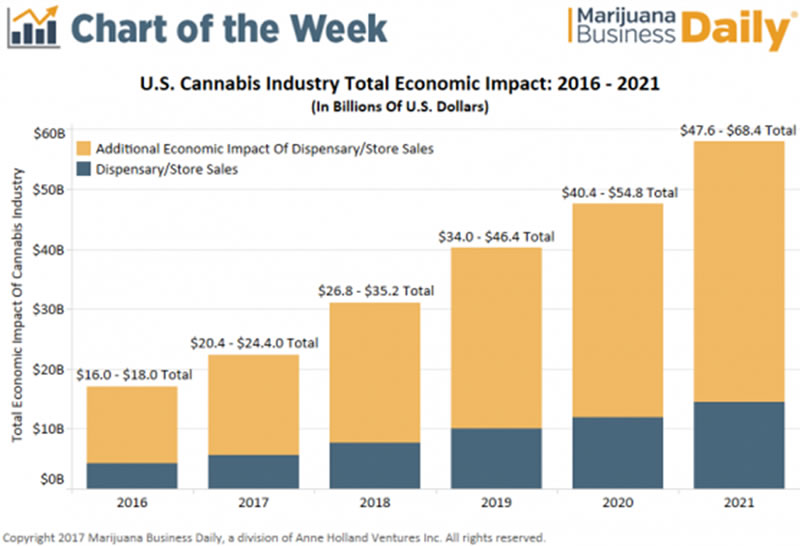

The economic impact is also significant. Last year there were approximately 121,000 workers in legal cannabis, and provided that the industry continues on its current trajectory, the number of people employed could reach 292,000 by 2021, according to research from ArcView Market Research and BDS Analytics.

With respect to the number of cannabis-related businesses, estimates project a total forecasted economic impact on the U.S. economy of between $47 billion and $68 billion by 2021, according to Marijuana Business Daily.

Source: Marijuana Business Daily

Industry Challenges

Cannabis and Banking

The federal status of marijuana has implications for private and public companies in banking as well. Both credit card companies and banks are reticent to support marijuana companies as clients, due to the lack of a federal mandate. Under federal law, banks must disclose marijuana-related transactions as suspicious activity. For banks, this could mean bringing unwanted federal attention and regulatory scrutiny if they choose to service the cannabis industry. As a result, large banking institutions are refusing to support cannabis-entrenched businesses. In fact, JP Morgan Chase & Co. and Bank of America have made it company policy to not work with the marijuana industry. Chase says that, “as a federally regulated institution, we don’t process payments for businesses participating in federally prohibited activities.” Some small independent banks, however, are open to getting involved. Following a 2014 directive from the Financial Crimes Enforcement Network (FinCEN), an arm of the Department of the Treasury, banks are allowed under law to service marijuana businesses as long as they comply with anti-money-laundering regulations.

As marijuana is illegal under federal law, the U.S. dual banking system, with both federal and state chartered institutions, becomes conflicted. Given that federal law enforcement and federal financial regulators have significant power and oversight with the ability to punish institutions that are non-compliant with federal statues, significant barriers exist. As cash businesses, companies large and small are left with the option of paying their employees, suppliers, and vendors in cash, in addition to paying their sales and income taxes in cash. An estimated 70% of cannabis businesses have no bank accounts, and losing your first banking relationship has become a rite-of-passage for those in the business of cannabis.

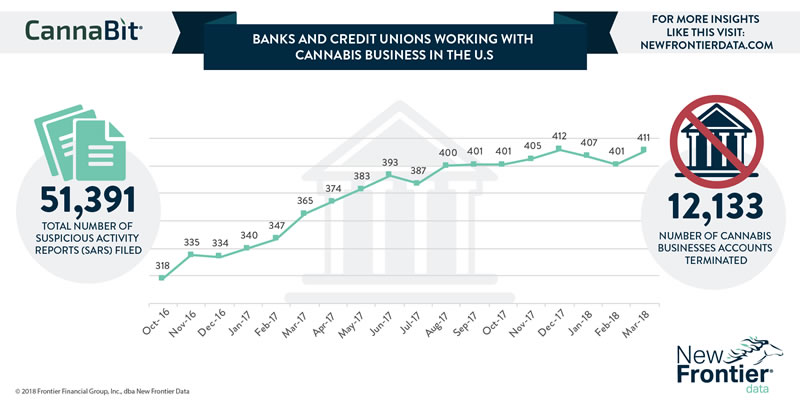

According to FinCEN’s Marijuana Banking Update, based on Suspicious Activity Report (SAR) filings, there were approximately 400 depository institutions actively providing banking services to marijuana businesses in the U.S. as of September 30, 2017. Less than 100 of those were credit unions, while the rest were banks. FinCEN’s data show that the agency received a total of 39,025 SARs using key phrases associated with marijuana-related businesses by the end September 2017.

Source: New Frontier Data

Cannabis and banking are a political game that has been an ongoing challenge to the industry. There are several pieces of legislation winding their way through the U.S. Congress that could potentially remove the current banking restriction and, more importantly, 280-E expenses currently disallowed by the IRS, as discussed below.

Taxes

Since cannabis remains designated as a Schedule 1 controlled substance by the U.S. government, many basic business expense deductions are not allowed on federal tax returns under Internal Revenue Code Section 280-E. Section 280-E, enacted in 1982, basically states that someone who is doing something that is illegal federally can only deduct their Cost of Goods Sold (COGS) for federal tax purposes. In short, Section 280-E prevents cannabis producers, processors and retailers from deducting any business expenses from their income, except for those considered COGS. Obviously, this inability to offset business expenses creates a hindrance for cannabis companies. Interstate commerce is also prohibited by the Schedule 1 classification. This puts a ceiling on both the ability to scale and the amount of growth businesses can achieve, because they are constrained by federal law, which discourages larger, publicly traded companies from participating in the industry.

There may be some paths to explore regarding court rulings. In the 2007 tax court case of Californians Helping to Alleviate Medical Problems, Inc. (CHAMP) v. The Commissioner, a California medical marijuana dispensary won its case against the IRS allowing medical marijuana companies to deduct expenses that could reasonably be separated from the trafficking of marijuana (as CHAMP offered caregiving services, education, and support for patients in addition to selling marijuana). Using Section 236-A, state-legal cannabis businesses are also allowed to capitalize on indirect costs like inventory and administrative costs, and state excise taxes where they can be deducted under COGS. As a consequence, marijuana businesses are required to determine what expenses are included in COGS and, therefore, what expenses are deductible. On January 23, 2015, the IRS released an internal legal memo which provided guidance to examiners on how Section 280-E should be applied in the cannabis industry. Per the memo, a retailer can include the invoice price of the cannabis, including transportation and other charges incurred in acquisition. A producer can include direct material and labor costs, as well as certain indirect costs such as depreciation, insurance and factory operational expenses in COGS. This memorandum, however, may not be used or cited by taxpayers or preparers as precedence.

Recently, the United States Court of Appeals for the Ninth Circuit ruled on Canna Care v. The Commissioner. The Court upheld the United States Tax Court’s ruling denying a California dispensary’s operating expense deductions under Section 280-E. The Tax Court held that, unlike CHAMP, Canna Care’s only business was selling cannabis, and therefore, none of its operating expenses could be deducted under Section 280-E. It should be noted, however, that the Ninth Circuit Court of Appeals did not rule on the merits of Canna Care’s 8th Amendment claim of excessive and burdensome fines, and it’s possible that a federal court might someday rule that the IRC 280-E is unconstitutional. Therefore, cannabis businesses that file a protective refund claim could theoretically recover taxes paid for that year.

Due Diligence: Evaluation, Valuation, and Investing

Medical marijuana and recreational cannabis company due diligence considerations are distinguished from pharmaceutical and biotech cannabis businesses in a few fundamental ways. The former companies are evolving in an ever-changing regulatory ecosystem, while the latter are guided by succinct FDA regulations and guidance. Cannabis companies, whether consumer packaged goods companies, retailers, growers, processors, analytical quality labs, ancillary service companies, or pharmacy dispensaries, do not lend themselves well to standard metrics and methods of evaluation or valuation. Multiples of revenue, EBITDA, Net Operating Profit, etc. in the cannabis economy have their own biases and predilections. When evaluating companies in today’s cannabis economy, it becomes necessary to reference the proper prevailing industry proxies for comparison and to handicap key performance criteria accordingly. Net Present Value of cash flows is not uncommon. With respect to performing due diligence on other business aspects, a well-developed strategic business plan, experienced senior executives with an appreciation of business risk, and a strong operating team with tactical business execution experience are key diligence rules that still apply.

A comprehensive plan should serve several purposes:

- As a strategic compass and internal planning road map; for tracking, coordination, reconciliation, accountability, etc.; and

- As the basis for an external marketing document that would serve as the core guiding document of any capital raise and in support of marketing to potential partners and targeted customers.

Seasoned executives from industries that parallel are consumer packaged goods and pharmaceuticals, where there is a proven discipline and strategic mind-set to rely upon. Industry knowledge (whether direct or parallel) and operating expertise go a long way to avoiding costly tactical mistakes. Whether potential strategic partner, investment target, or other, the key to the due diligence formula is identifying those cannabis companies with proven players that have the potential to navigate the landscape and to excel.

Compliance

The cannabis business is in the early stages of creating an ultra-compliant industry where anyone who deviates from the path set by the state will be viewed, essentially, as a bad actor. Those who have been in the industry for a while will need to accept this as the new reality. As for new entrants to the cannabis marketplace, strict compliance to state policies should be a primary focus. Self-Regulation Organizations (SRO) are starting to emerge. SROs not only need to be mindful of their own businesses, but also pay attention to compliance issues from many different regulatory bureaus. They may include:

- Financial: SEC, FinCen

- IRS

- FDA

- State and city planning/zoning

- State business licensing

- State/local health codes

- EPA/local/state environmental agencies

Conclusion

Despite continued federal opposition to legalization, burdensome tax rules at both the federal and state-levels, and complexities to valuation, “cannabusiness” is beginning to thrive. Many see opportunity as they drive their way through the twists and turns of state-by-state regulations in a forbidding federal landscape. Cannabis has so far demonstrated that it has the potential to create jobs, contribute to economic growth, and provide tax revenues where the product is permissible. Suffice to say, the navigational guidance and diligence of industry experienced professionals is well worth deploying.

About the Author

Leslie Bocskor is the President of Electrum Partners, a business advisory services company in the legal cannabis industry. Please direct inquiries to the Contact Us form on our website. www.electrumpartners.com/

Contributors

Jonathan Berlent is CEO of Trulee Health, a vertically integrated telemedicine pharmacy product and services company focused on women and men’s health and wellness. Email: [email protected]; website: www.TRULEEHEALTH.com

Marni Pankin is a Partner in the Firm’s national Alternative Investment Industry group, responsible for advising clients on the formation and operation of investment funds.

How Marcum LLP Can Help

Given the varying state regulations and state and federal tax implications, now is a good time for professional investors, operating companies, and ancillary services organizations conducting business in the fast growing yet fluid regulatory environment of the cannabis arena to contact Marcum LLP. Marcum LLP provides tax, audit, and business services to clients in multiple cannabis-related industry sectors and jurisdictions.