Five Proven Strategies to Tackle Estate Taxes

By Gregory Lopez, President, Marcum Insurance Services

Although only 0.07% of U.S. taxpayers will pay any estate tax, those subject to paying the tax face challenges around how to best fund the looming obligations for liquidity.

The main pathways to funding estate taxes are highlighted in this article, along with their corresponding costs and characteristics. To understand how best to fund estate taxes, let’s first understand who will be subject to the estate tax and to what extent.

THE ESTATE TAX LANDSCAPE

Estate tax filing is required if the gross estate of a decedent(s), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is valued at more than the filing threshold for the year of the decedent’s death. The table below illustrates these thresholds for a single taxpayer. Typically, a married couple would each have access to this exemption, doubling the total exemption amount. The current estate tax is assessed at 40% of the amount in excess of the allowable exemption in the year of death.

| Total Taxable Estate | $40,000,000 |

| Spouse 1 Exemption in 2023 | $12,920,000 |

| Spouse 2 Exemption in 2023 | $12,920,000 |

| Taxable Estate | $14,160,000 |

| Estate Tax Due | $5,664,000 |

This example illustrates the taxes due for a married couple who both died in 2023 with an estate value above the exemption. Taxes due would be approximately $5,664,000.

ESTATE TAX FUNDING OPTIONS

Year of Death |

Lifetime Exemption Amount |

|---|---|

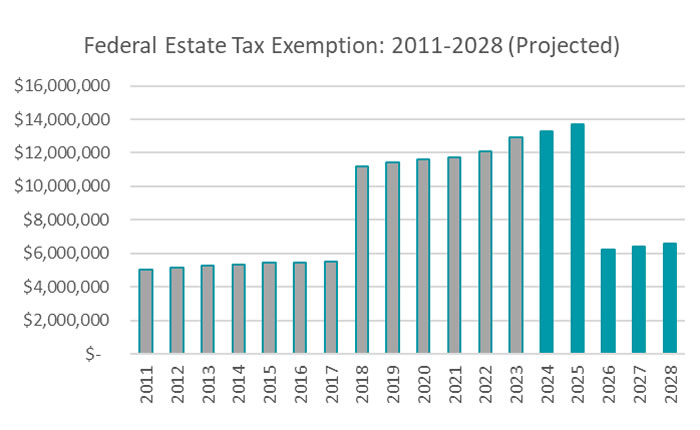

| 2011 | $5,000,000 |

| 2012 | $5,120,000 |

| 2013 | $5,250,000 |

| 2014 | $5,340,000 |

| 2015 | $5,430,000 |

| 2016 | $5,450,000 |

| 2017 | $5,490,000 |

| 2018 | $11,180,000 |

| 2019 | $11,400,000 |

| 2020 | $11,580,000 |

| 2021 | $11,700,000 |

| 2022 | $12,060,000 |

| 2023 | $12,920,000 |

Cash or securities

This may be the most straightforward way to pay for estate taxes. This method allows the taxpayer to wait and see what the estate tax will be and direct trustees, beneficiaries, or (in some cases) spouses to handle the issue at the time of the obligation. This method assumes we expect to have the cash or cash equivalents to make estate tax payments. In general, the estate tax is due within nine months2 after death.

Pros

This method can provide a step-up in basis if appreciated assets used for estate taxes are in the taxable estate. (It is important to note that irrevocable trusts are not granted the provision for a step-up in basis.)

Cons

As we have seen over the years, yields on money markets, bonds, CDs, and other fixed assets experienced a prolonged environment of low rates. In fact, 1-month and 3-month Treasury bills yields dipped below zero in March of 2020. Periods with low interest rates caused a deterioration in the buying power of these assets due to interest crediting rates staying below the inflation rate.

All time high tax exemptions are expected to sunset in 2026. Assuming 3% inflation, exemptions are projected to reduce to $6,000,000. Taxpayers with a projected estate tax due have a window of opportunity for additional planning before the high exemption sunset.

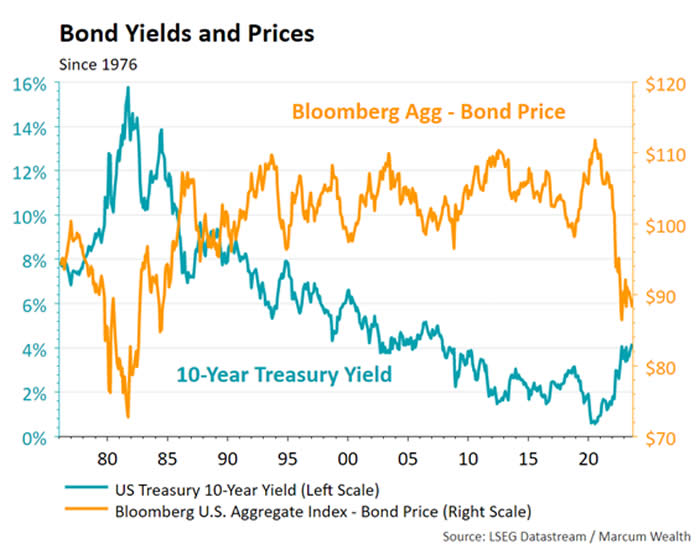

At the end of 2022, we experienced the effect of rising rates. Bond values decrease in a rising interest rate environment, especially where rates rise quickly. As of September of 2023, the U.S. Aggregate Bond index has experienced a negative 3-year cumulative return of -14.16%. The chart below illustrates this example:

If your estate taxes are due at a time when you are invested in a bond portfolio, there is a potential that your estate tax reserve could be lower than anticipated and require the liquidation of assets you may not be planning on liquidating.

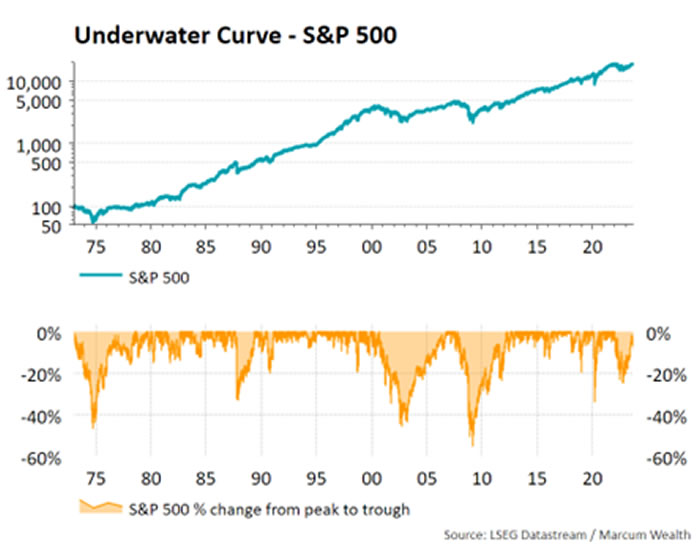

Planning to sell marketable securities like stocks, mutual funds, or ETFs to fund a looming estate tax comes with its own risks. Primarily, if timed poorly, market fluctuations and bearish cycles could also leave a taxpayer with less liquidity for taxes than anticipated. The chart below shows the growth of the S&P since 1970. Notice the S&P’s trend has been upward, but market cycles create drawdowns. The drawdowns are highlighted at the bottom of this graph, and they range in both the severity of the trough/loss and the duration of time before getting back to the previous market peak.

Forced Sale of an Asset

If an estate does not have liquid assets to pay the estate tax, it will be forced into selling illiquid assets. The short window to pay the government can result in these assets sold at severely discounted values. That may cause the estate to sell more assets than expected to fund the tax, placing a greater liquidity burden on the estate and reducing the assets left to heirs and charities. Other concerns are the illiquidity of certain asset categories such as real estate, private business interests, and others.

Consider the following example. Ted is divorced and owns a second-generation manufacturing business. He plans to pass the company down to his son. Ted’s business is his main asset, as he has been investing profits back into the business. Because of his reinvestment in growth, Ted does not have a large pool of liquid cash or securities. Ted dies after a short bout of pancreatic cancer, and his estate owes roughly $20,000,000 in estate taxes for the right to pass the business to his son, Philip. Philip is faced with the reality of having to sell some of his business interests to raise the cash or take on debt at historically high interest rates. If selling a portion of the business is the best option, the sale may take a great deal of time, and he may not be offered full fair market value for the business because Ted was integral to the business’s success.

If the forced sale is real estate, a market decline and high interest rates may negatively affect the value received. In addition, real estate transactions may take more time than the allowable window for tax payments.

Use a Loan to Pay Estate Tax

To avoid the forced sale of illiquid assets like a private business or real estate, an estate may borrow against its assets to pay the tax due. This can effectively maintain family ownership in closely held businesses and may also benefit the estate. Loan interest from loans to pay estate taxes may be deductible in certain circumstances. It may also be possible for a lump-sum deduction to be taken for estimated future interest payments.

The Intra-Family Loan. A popular alternative to a commercial lender involves obtaining a loan from another family-owned entity to pay the estate tax due on less liquid assets. The advantage of such an arrangement is summarized by the difference in potential tax savings to the estate and the income tax owed by the entity receiving interest payments.

One problem that may arise when using debt as a tool for paying estate taxes is that debt markets may not be favorable at the time of taxes due. As recently as this year (2023), we have seen banks tighten lending standards for businesses and households. Some regional banks have all but lost their ability to lend to middle-market companies. If a commercial bank can extend a loan, the other variable to consider is the interest rate, many of which have hit record highs. If the loans are required to fund a business transfer to the next generation, excessive debt could be a drag on the business and have the potential to result in long-term negative growth and performance.

§6166

Under very specific circumstances, an estate may qualify for a 5-year deferral followed by a 10-year installment plan. The language of §6166 is strict in determining if an estate qualifies for the extension, and the utilization of this option is complex. The opportunity to defer under §6166 applies only to owners of closely held companies when the value of the taxpayer’s interest exceeds 35% of the Adjusted Gross Estate. Only the tax attributable to the value of the business may be extended under this section.

Caution: A tax lien may be placed on the assets held in the estate until the tax has been completely satisfied. This can inhibit the company’s ability to obtain other debt needed in the regular course of its business. This strategy also requires faith that the government will continue to provide this option many years in the future and, as such, may not be a reliable source of relief.

Purchase Life Insurance

Often, one of the most efficient ways to fund a future liability at death is to prepare for it now. The tax-free death benefit from life insurance is not only economical but also holds the power to eliminate unnecessary stress for you and your heirs worried about paying the estate tax. Beneficiaries are provided with immediate liquidity to pay the estate tax, eliminating the need to apply for loans, petition the IRS for relief, or sell off assets at an unfavorable time.

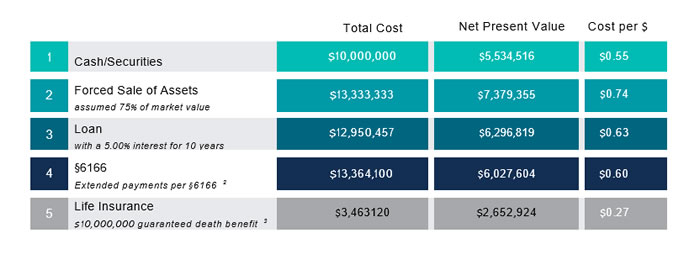

The chart below shows the per-dollar costs of each option for funding the estate tax.

Assumed death in 20 years with a net taxable estate of $25,000,000 and a 40% tax rate

1 – Using a 3.00% discount rate.

2 – The company’s value is assumed to be 80% of its overall net worth, and the portion of estate taxes that are not eligible for §6166 are to be paid immediately. IRS underpayment interest of 5.00%. Not all estates will qualify. Above is an estimate only and will depend on the IRS’s stance on utilizing this provision at the time of death.

3 – Average premium of top 10 carriers to provide $10,000,000 of guaranteed death benefit for life.

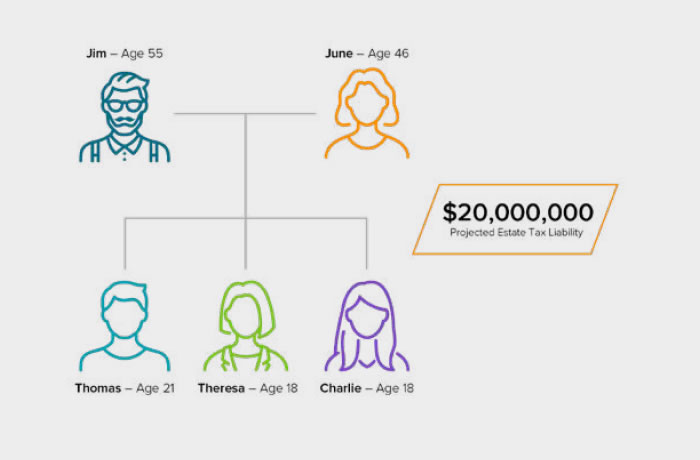

Consider the following example:

Jim and June are a married couple with three adult children. They anticipate paying estate tax and are weighing the options of funding the liability.

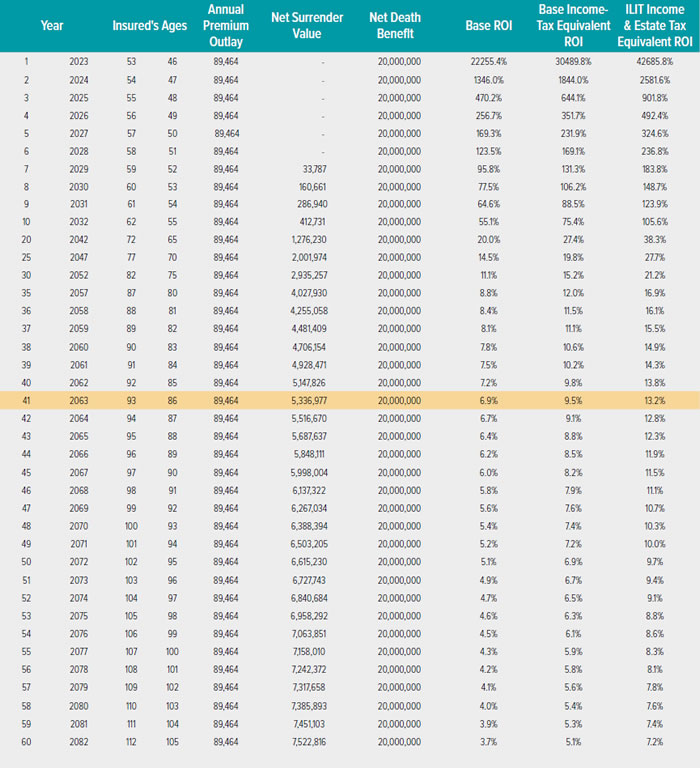

Jim and June settle on using life insurance to fund their estate tax obligations. A healthy couple like them can support a policy to provide for a death benefit, often contractually guaranteed to pay at the surviving spouse’s death. This is known as a survivorship policy and can require lower annual premiums than a policy underwritten on a single life. Jim and June have a taxable estate but are not using their annual gift tax exemption, which is currently $17,000 (2023) per spouse, per beneficiary. With three beneficiaries, they have a total of $102,000 of available gifting per year, which does not count against their lifetime exemption. Since the premiums are lower than this number, they establish an irrevocable life insurance trust to own the policies and gift the premiums on an annual basis. The trustee will make the premium payments.

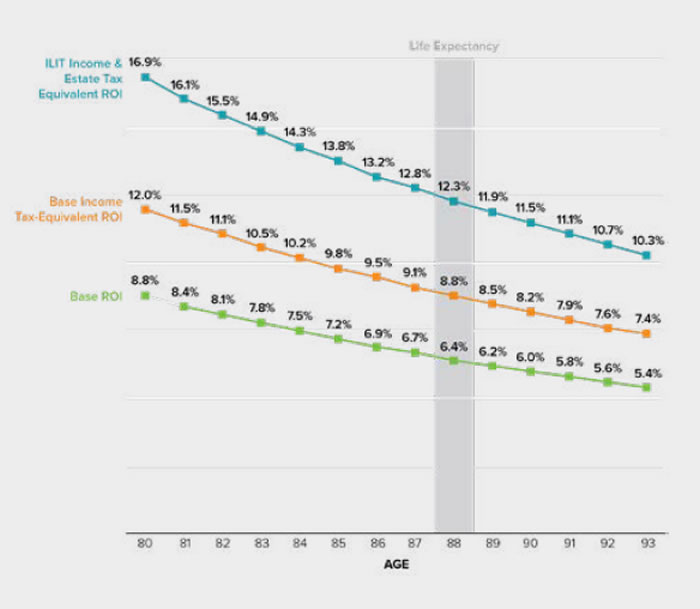

This was a desirable option for several reasons. As seen above, the internal rate of return for the policy at life expectancy is very attractive. On top of that, the life insurance death benefit is not subject to ongoing income tax. It pays tax-free, enhancing the tax-equivalent life insurance death benefit internal rate of return. And, since the couple used in-estate dollars to gift the policy premiums, they turned assets that would be taxed at 40% into assets that would not be taxed upon their death. This increases the Income and Estate taxable equivalent of the death benefit to an attractive level.

Ultimately, there are many ways to pay for the estate tax. Each comes with its limitations, benefits, and drawbacks. It is up to you and your advisors to understand all of these factors and determine the best plan of action for you and your family.

Tax")