An Explanation of the Asset Approach to Valuation

By Sean R. Saari, Partner, Advisory Services

An excerpt from Marcum’s “How a Company is Valued” e-book

Investors in publicly-traded companies have the luxury of knowing the value of their investment at virtually any time. An internet connection and a few clicks of a mouse are all its takes to get an up-to-date stock quote.

Of all U.S. companies, however, less than 1% are publicly-traded, meaning that the vast majority of companies are privately-held. Investors in privately-held companies do not have such a readily available value for their ownership interests. How are values of privately-held businesses determined, then? Each month, this eight blog series will answer that question by examining a key component of how ownership interests in privately-held companies are valued.

Asset Approach

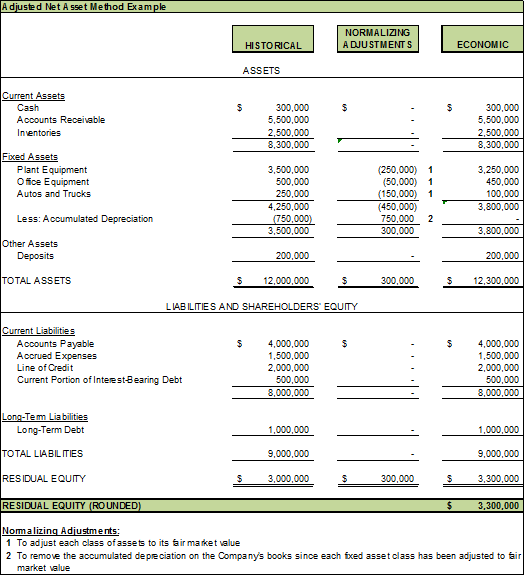

The most commonly utilized asset-based approach to valuation is the Adjusted Net Asset Method. This balance sheet-focused method is used to value a company based on the difference between the fair market value of its assets and liabilities. Under this method, the assets and liabilities of the company are adjusted from book value to their fair market value, as presented in the example below:

As shown above, adjustments are made to the company’s historical balance sheet in order to present each asset and liability item at its respective fair market value. Examples of potential normalizing adjustments include:

- Adjusting fixed assets to their respective fair market values;

- Reducing accounts receivable for potential uncollectable balances if an allowance for doubtful accounts has not been established or if it is not sufficient to cover the potentially uncollectable amount; and

- Reflecting any unrecorded liabilities such as potential legal settlements or judgments.

Consideration of the Adjusted Net Asset Method is typically most appropriate when:

- Valuing a holding company or a capital-intensive company;

- Losses are continually generated by the business; or

- Valuation methodologies based on a company’s net income or cash flow levels indicate a value lower than its adjusted net asset value.

One needs to keep in mind that when income or market-based valuation approaches indicate values higher than the Adjusted Net Asset Method, it is typically dismissed in reaching the concluded value of the company. This is because income and market-based valuation approaches provide a much more accurate reflection of any goodwill or intangible value that the company may have.

The Adjusted Net Asset Method does not necessitate the actual termination or liquidation of the business (renowned valuation expert Shannon Pratt believes some analysts mistakenly confuse the use of an asset-based approach with a liquidation premise of value). Rather, the Adjusted Net Asset Method can be used with all premises of value including value-in-use as a going concern business enterprise.

To summarize, the Adjusted Net Asset Method is a balance sheet-based approach to valuation that is relied upon most often for holding companies and companies generating losses (or only modest levels of income in relation to their net assets).

Questions? Contact Sean R. Saari, Partner, Advisory Services.